Business Is Streamlining The Industry But Its Parts Are Not")

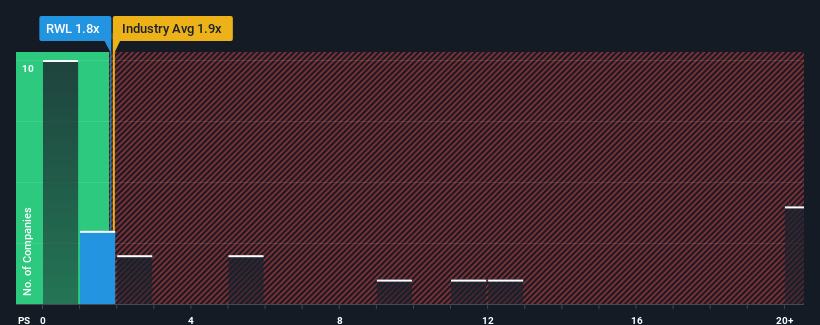

It’s not deep to say that Rubicon Water Limited’s (ASX:RWL)’s price-to-sales (or “P/S”) ratio of 1.8x now seems relatively “middle of the road” for companies in the Australian Electronics industry, where the median P/S ratio is 1.9x. However, investors may miss a clear opportunity or potential pullback if there is no rational basis for the P/S.

Check out our latest analysis for Rubicon Water

How Rubicon Water Performs

For example, Rubicon Water’s declining revenue in recent times should be food for thought. Perhaps investors believe that recent earnings performance is enough to keep the industry in line, preventing the P/S from falling. If not, then existing shareholders may be a little nervous about the share price recovery.

Want the full picture of revenue, income and cash flow for the company? Then ours free The report on Rubicon Water will help you illuminate its historical performance.

How Are Rubicon Water’s Profits Growing?

To justify its P/S ratio, Rubicon Water needs to generate industry-like growth.

In reviewing the last financial year, we were disheartened to see that the company’s revenues fell to the tune of 18%. This means that a decline in income is also seen in the longer term as income has decreased by 6.7% in total over the last three years. Therefore, it is reasonable to say that the recent revenue growth is not desirable for the company.

Weighing that medium-term earnings trajectory against the industry’s one-year forecast for an expansion of 13% shows that it’s a bad look.

With this information, we know that Rubicon Water is trading at a similar P/S compared to the industry. Apparently many investors in the company are much less bearish than they have shown in recent times and are not ready to let go of their stock right now. There is a good chance that shareholders are setting themselves up for future disappointment if the P/S falls to levels more consistent with recent negative growth rates.

The Key Takeaway

We can say that the power of the price-to-sales ratio is not primarily as a valuation instrument but to measure current investor sentiment and future expectations.

We unexpectedly see that Rubicon Water trades at a P/S ratio comparable to the rest of the industry, despite experiencing a decline in earnings during the medium-term, while the industry as a whole is expected to grow. Although it is in line with the industry, we are not comfortable with the current P/S ratio, as this poor earnings performance is unlikely to support a more positive sentiment in the long term. Unless recent medium-term conditions improve significantly, investors will find it difficult to accept the share price as fair value.

Don’t forget that there are other risks. For example, we know 2 warning signs for Rubicon Water (1 is not very good to us) you should know.

If you uncertain of Rubicon Water’s business viabilitywhy not explore our interactive list of stocks with strong business fundamentals for other companies you may have missed.

Have feedback about this article? Worried about content? Contact with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This Simply Wall St article is general in nature. We provide commentary based on historical data and analyst forecasts using only an unbiased approach and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take into account your goals, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any of the stocks mentioned.

Join a Paid User Research Session

You will receive a US$30 Amazon Gift card for 1 hour of your time while helping us build better investment tools for individual investors like yourself. Sign up here